Oil Crashes 31% in Worst Loss Since 1991 After Price War Erupts

Oil Price Crisis?

(This is a repost from my original blog on March 9, 2020)

Any saving grace to the kind of news above? With a looming recession as corona virus spreads worldwide, the price war in oil sends the possibility of crude into US$20! This is indeed a double whammy to what the fragile market could handle.

However, what I’m going to share next (I hope), can be a silver lining among the dark clouds. Occidental Petroleum Corporation (OXY), a company that engages in the acquisition, exploration, and development of oil and gas properties in the United States, the Middle East, and Latin America. The company operates through three segments: Oil and Gas, Chemical, and Marketing and Midstream.

Occidental’s wholly owned subsidiary OxyChem manufactures and markets basic chemicals and vinyls.

Primary areas of focus include:

Oil & gas

Chemical

Midstream and marketing that involves in purchases, markets, gathers, processes, transports and store hydrocarbons

WES (an independent partnership)

What Happened to Occidental Petroleum (OXY) Recently?

It has been in the news lately and its share prices have been in the downward trend in 2019. As of the writing today, it tanked 52% to US$12.51 [9-Mar-2020]. Talk about a good margin of safety!

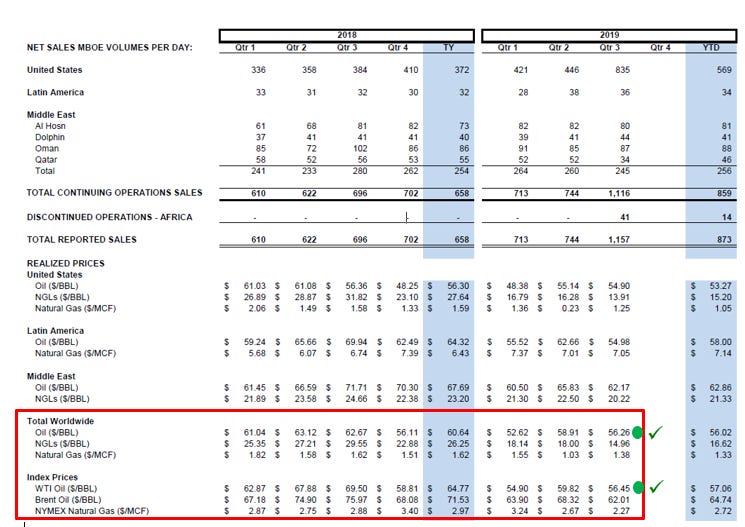

OXY reported earnings missed estimates for Q3 2019 which primarily due to the M&A cost from acquisition of Anadarko, however the total revenue were 3.2% better from estimate. The production volume also increased due to higher drilling activity and solid output from the Permian Resources region.

Nevertheless, world wide crude oil prices decreased 10.2% year over year to $56.26 per barrel which did not allow the company to realize full benefits of higher production and sales volumes in the reported quarter.

The acquisition deal with Anadarko Petroleum has be deemed as a bad move by theby investors, particularly activist investor Carl Icahn. Management believes it’s a good move. which cause the market sentimental to swing downward trend.

Source: https://www.oxy.com/investors/Documents/Earnings/OXY3Q19EarningsPressRelease.pdf

OXY has also been selling non-core assets, as well as embarked on a headcount reduction – these activities will increase cashflow and reduce operating costs going forward.

The market sentiment pretty much driven by the overwhelming lime lights the multi-millions dollar analysts shine on the company. Given the fact that the share price has been downward trend since the decrease of crude oil prices; investors has been struggling to have faith especially post the acquisition of Anadarko with such a high price. The merger was controversial as it significantly raised Occidental’s debt levels which fear the investors more on the maturity of the near-term debt.

However, based on the Q3 earning call the CEO of OXY has been clearly stated that the company has repaid $5bn in debt in the most recent quarter and does not have any maturities scheduled in 2020.

What Will happen to Its Future?

OXY revenue has been consistently increased from 2015 to-date.

Quoted: Seeking Alpha, Occidental Petroleum and left Brain

The company operates through the following segments:

The Q3 2019 sales volume has been trending upwards by >60% vs same period last year.

The OXY Worldwide Oil/BBL price vs WTI Index is not very far off which means once the synergy is recognized with the breakeven point of $40/BBL it will drive significant increase to the operating margin for the company.

Occidental is reducing their stake in WES to under 50%. This paves the way for Oxy to pare down their stake in WES in future. Further, the reduction in shareholding means WES’ debt does not have to be consolidated into OXY’s books

Looking at the management, CEO Vicki Hollub with 30+ years career in Permian in various roles from Drilling Engineer to Area AP for OXY is absolutely the right person to integrate these companies. The acquisition of Anadarko (APC) will make OXY to be the largest market player in the industry.

Next, the Chairman Eugene Batchelder has a pretty good oilfield pedigree whom was the ConocoPhillips (COP) CFO in 2012 (COP is a role model of what a modern super major oil company should be).

OXY has a consistent track record of paying and growing dividends. Specifically, OXY has been increasing and paying dividends consecutively for the past 17 years. There are reasons to believe that OXY could be able to continue paying and increasing its dividend in the years ahead:

Occidental Petroleum’s management team is committed to protect OXY’s ability to continue paying dividends. Management had consistently reiterated that one of their main goal is to ensure that shareholders’ dividends are protected. In a recent interview, CEO Vicki Hollub alluded to the following: “The substantial free cash flow we will generate in higher price environments, combined with our ability to pay a sector-leading dividend throughout lower commodity price environments, is unmatched”. This clearly indicates management’s commitment towards ensuring a sustainable and industry-leading dividend

Occidental Petroleum has been diversifying non-core assets to pare down debt, reduce interest expenses and increase free cash flow from operations. In addition, OXY had previously offered a group of employees the option of voluntary termination, and had recently instituted a company-wide non-voluntary termination program, to ensure that it operates on a lean and efficient workforce. All these activities are likely to increase OXY’s free cash flow, which will go a long way towards ensuring dividend payments are not disrupted; and

Occidental Petroleum had put in place hedges to ensure that dividend targets can continue to be met even in an low oil price environment. In fact, at USD 40 bbl, OXY is able to breakeven and maintain dividends, while at USD 50 bbl, OXY is able to maintain dividends, as well as grew production at 5% to 8%. The low production cost is extremely important, as it allows OXY to remain profitable in low price environments while other drillers are struggling to stay afloat, especially in a time of oil crisis like now! Drillers that do not survive under harsh conditions will reduce the competition that efficient producers such as OXY have to face. This allows 1. OXY to potentially acquire distressed assets at fire-sale prices and 2. Reduce overall crude oil supply and drive prices upwards.

Another reason to consider is that many shale producers are able to drill for crude oil, but do not have the capacity to transport the production obtained. Occidental Petrolem Corporation not only has sufficient pipeline takeaway and export capacity to transport its own production, but has spare capacity to derive revenue from transportation of production for other drillers.

Moreover, OXY’s current market cap is equivalent to its market cap prior to the acquisition of Anadarko. In a nutshell, at today’s prices, an investor is basically getting one company (i.e. Anadarko) for free.

My take is to hold Occidental Petroleum for now and watch out for the OPEC guys to agree on the production volume and oil price to hold steady at least above US$30/barrel. Once the coast is clear, with the potential upside from the recent merger, the large margin of safety of at least 50% from the price which Warren Buffet had bought into and the consistency in dividend payout; OXY will be a company that I would like to add into my portfolio.

If you want to learn more about how to find cheap and good stocks to generate passive income for you, click on the picture below to join Cayden’s Free Value Investing Masterclass now!